Setting Tax Rates: Corporate Tax and Sales Tax

In this article

Taxes are a fact of life in business, so you need to include a reasonable estimate for them in your forecast. Don't stress too much about this, though. This is business planning, not tax planning. The taxes we’re talking about here are theoretical expenses based on theoretical profits. It would be silly to get too specific about the details. Just set your standard rates to make sure that your forecast includes basic tax coverage.

NOTE: If you're looking for employer taxes, please update the Benefits & tax rates in the personnel forecasts.

Do I need to include Taxes in My Revenue Streams?

There's no need to add any tax amounts to your revenue stream entries. Just enter the actual revenue numbers with no tax added. The system will calculate your taxes and add them to the forecast automatically.

Setting Tax Rates:

- 1

-

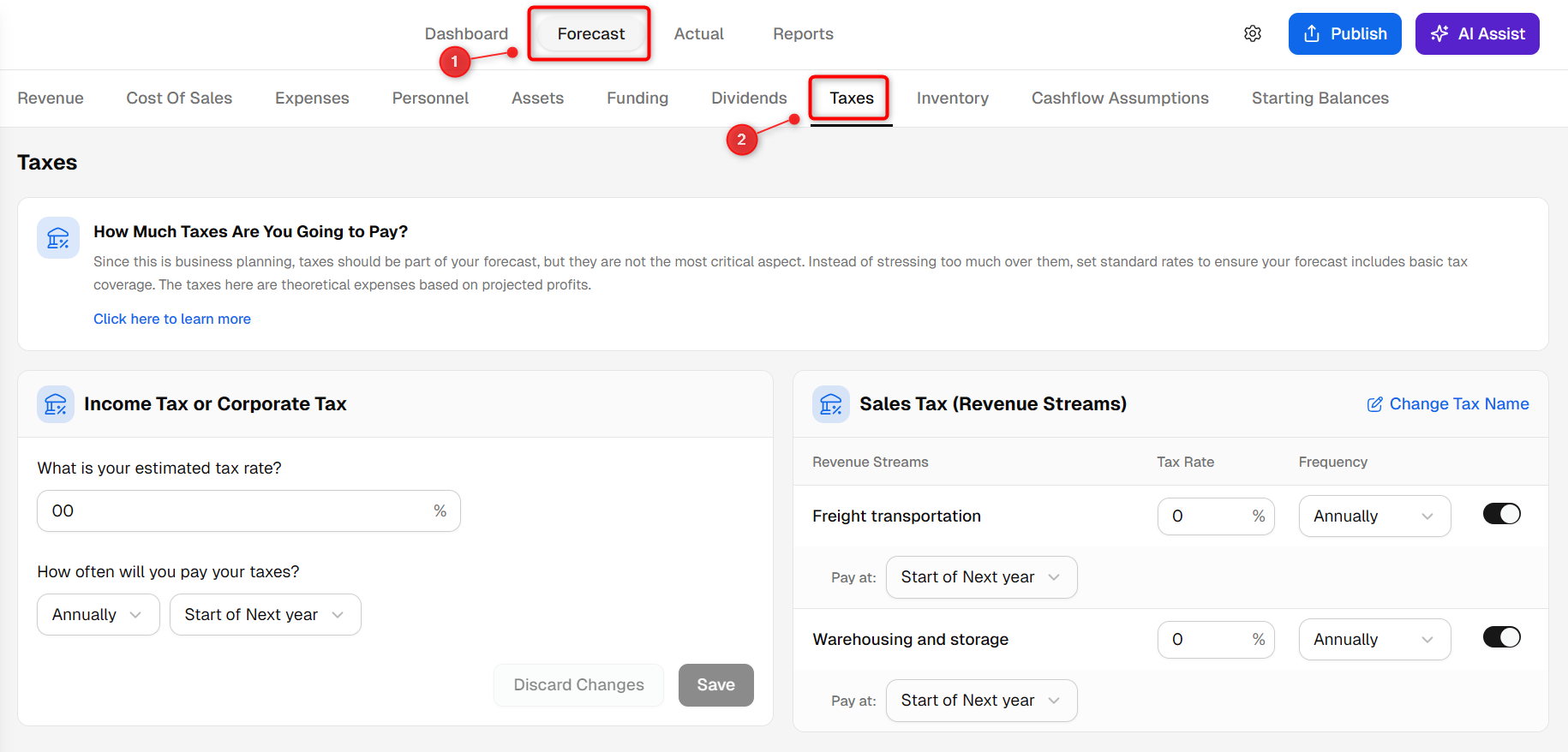

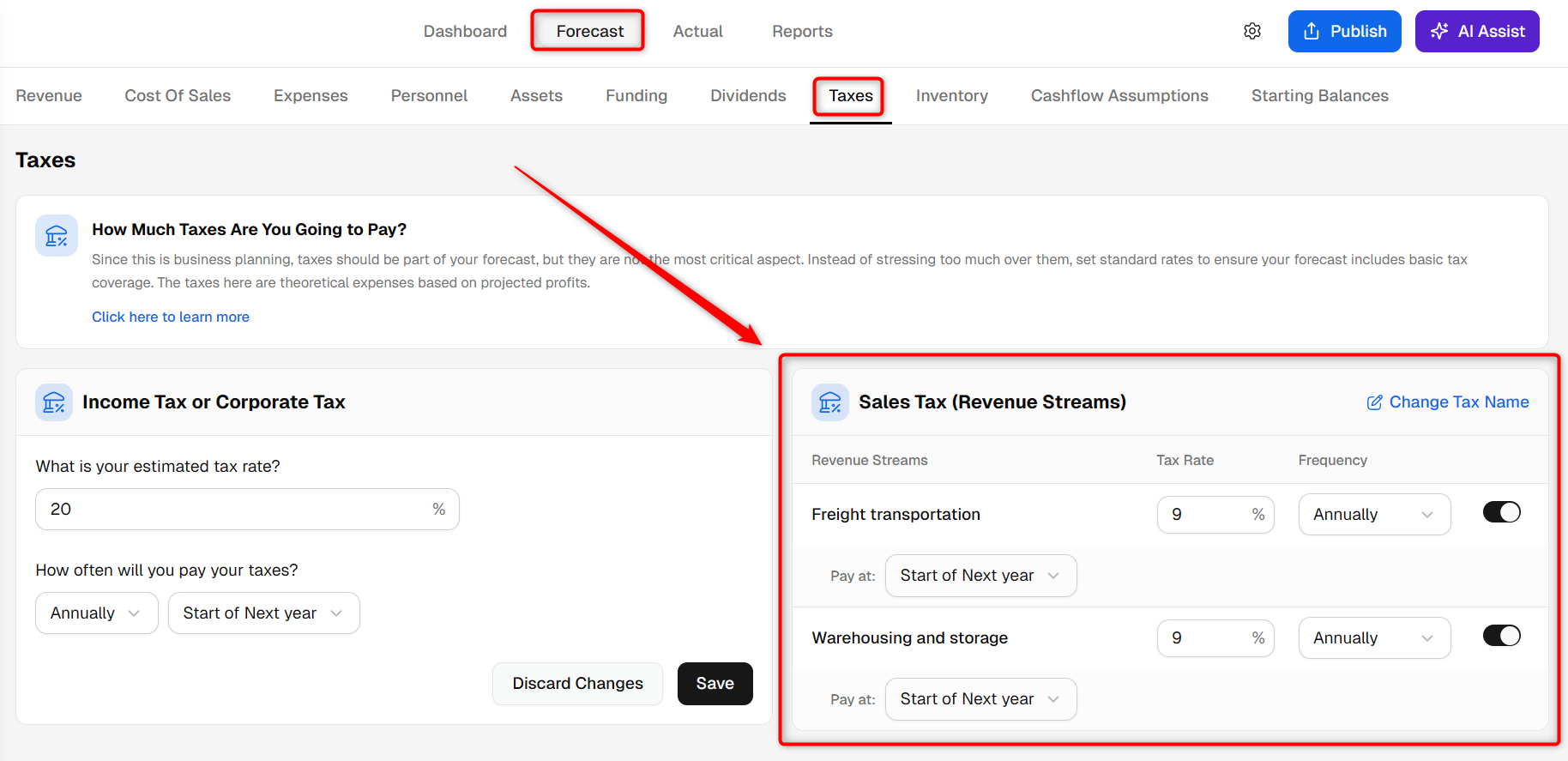

In your Finance Forecasting Module, access the 'Forecast' Tab. Then choose 'Taxes' to configure your tax rates.

- 2

-

Set Corporate Tax (Income Tax) Rates:

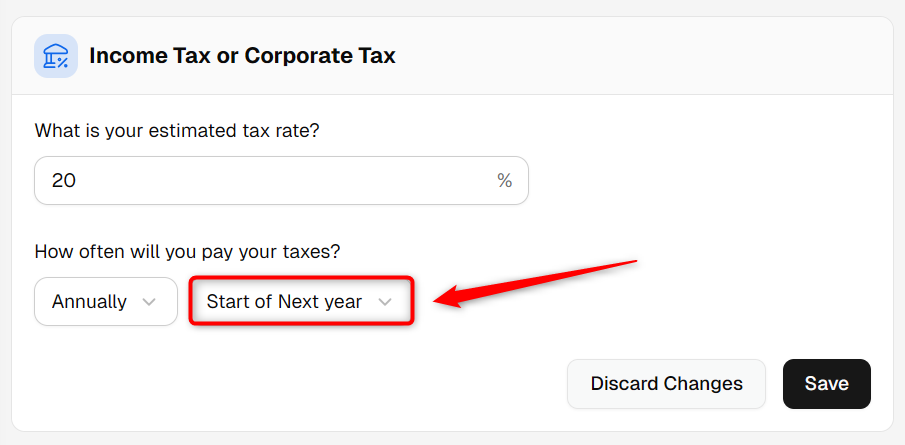

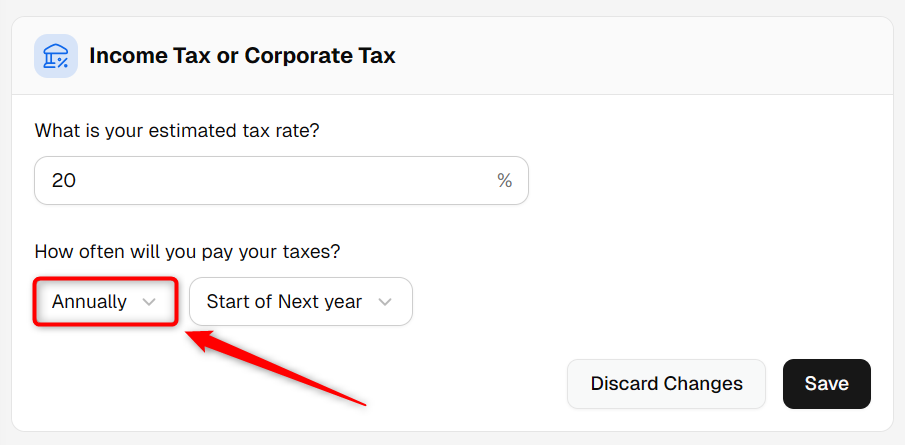

If your business is profitable in a given year, you will need to pay income taxes on that profit. Enter an overall tax rate. This estimated rate should cover all applicable income taxes — federal, state, local, etc. If you're not sure what to put, though, a 20% rate is probably close. It helps to keep in mind that income taxes typically apply only in periods when your business is profitable.

Note that this rate is only for income taxes. Employee-related taxes, like payroll and social welfare taxes, are covered on the Personnel page. Other taxes, such as property taxes, are generally best added as regular expenses.

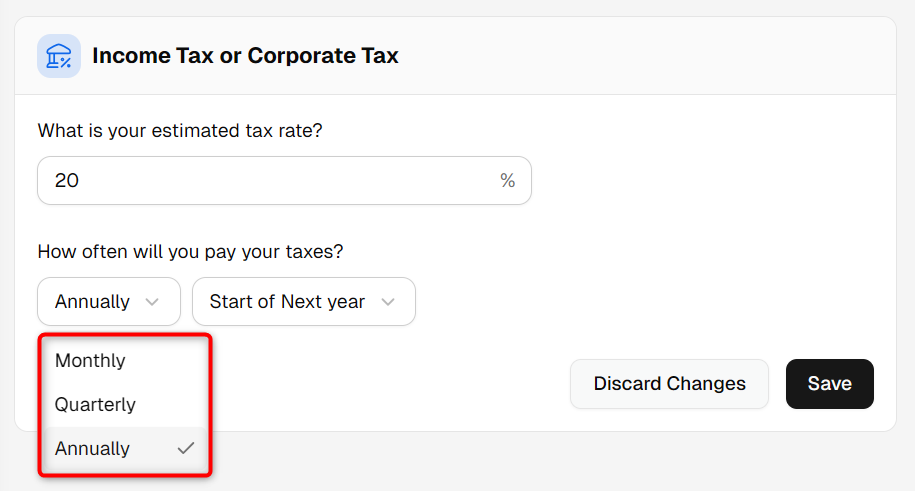

- Under the corporate tax section. Enter your estimated corporate tax rate (%), indicate how often you'll pay taxes (every month, or once per year), and you can also set the tax applicable time as below:

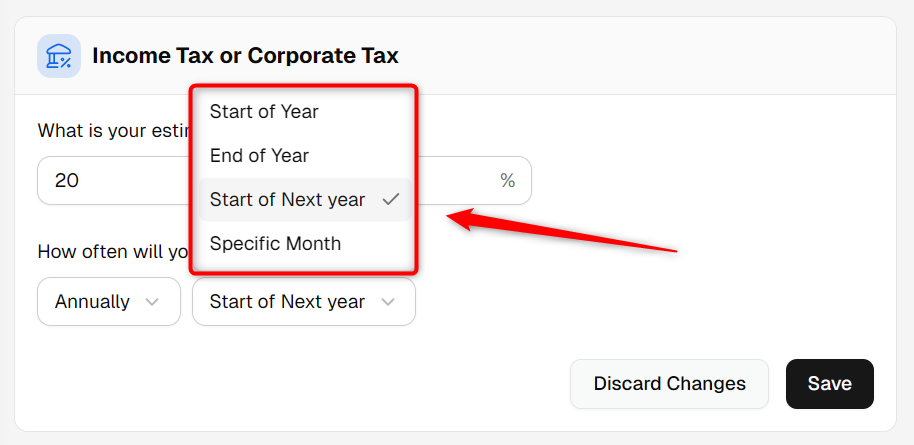

- Choosing When to Pay Your Taxes: When setting up corporate tax rates, you have the flexibility to specify when the tax should be applied. This can be crucial for aligning your tax obligations with your fiscal year and cash flow planning.

Here are the options available:

- Start of Year: Pay taxes at the beginning of the fiscal year, freeing up the rest of the year's cash flow and ensuring early compliance.

- End of Year: Defer tax payments until after all financial events of the year have been recorded, allowing for precise tax calculations and strategic financial management.

- Start of Next Year: Postpone tax payments to the beginning of the next fiscal year, aiding in cash flow management and year-end financial adjustments.

- Specific Month: Opt to pay taxes in a specific month that aligns with seasonal revenue peaks, optimizing cash flow management during financially robust periods.

-

After selecting suitable options, click on save button.

- 3

-

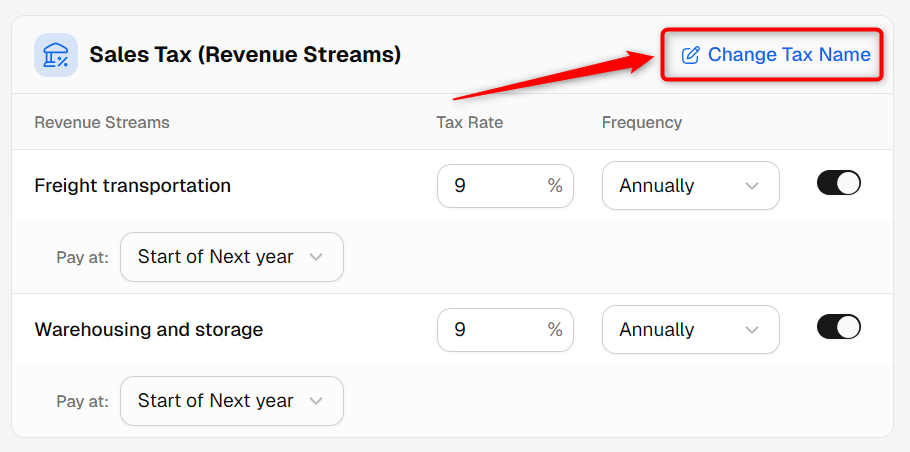

Set Sales Tax Rates:

Some companies need to collect sales taxes from their customers. This might include a national general sales tax (GST), value-added tax (VAT), or other national, state, or local sales taxes. This sort of tax collection will not affect your profitability since you are obliged to pay the collected taxes to the government on a regular schedule. But it will affect your cash flow projections for the time between when you receive the revenue and when the taxes are due to the government. It's important not to treat collected tax money as readily available cash.

NOTE: This step won't appear if you don't have any revenue streams in your forecast.

- On the Sales tax section, navigate to any revenue stream for which you will collect sales tax.

-

Enter the sales tax rate (%) that you will charge your customers:

- Indicate how often you'll pay taxes (every month, quarterly, or annually):

-

System auto-saves the changes.

-

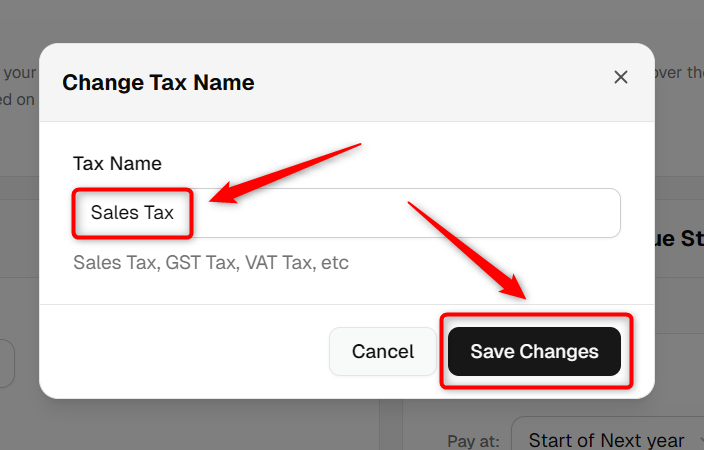

You can change the tax name as per requirements (e.g. VAT, GST etc.) form the Change Tax Name option.

TIP: To add your sales tax due from previous periods, refer to this step-by-step guide.

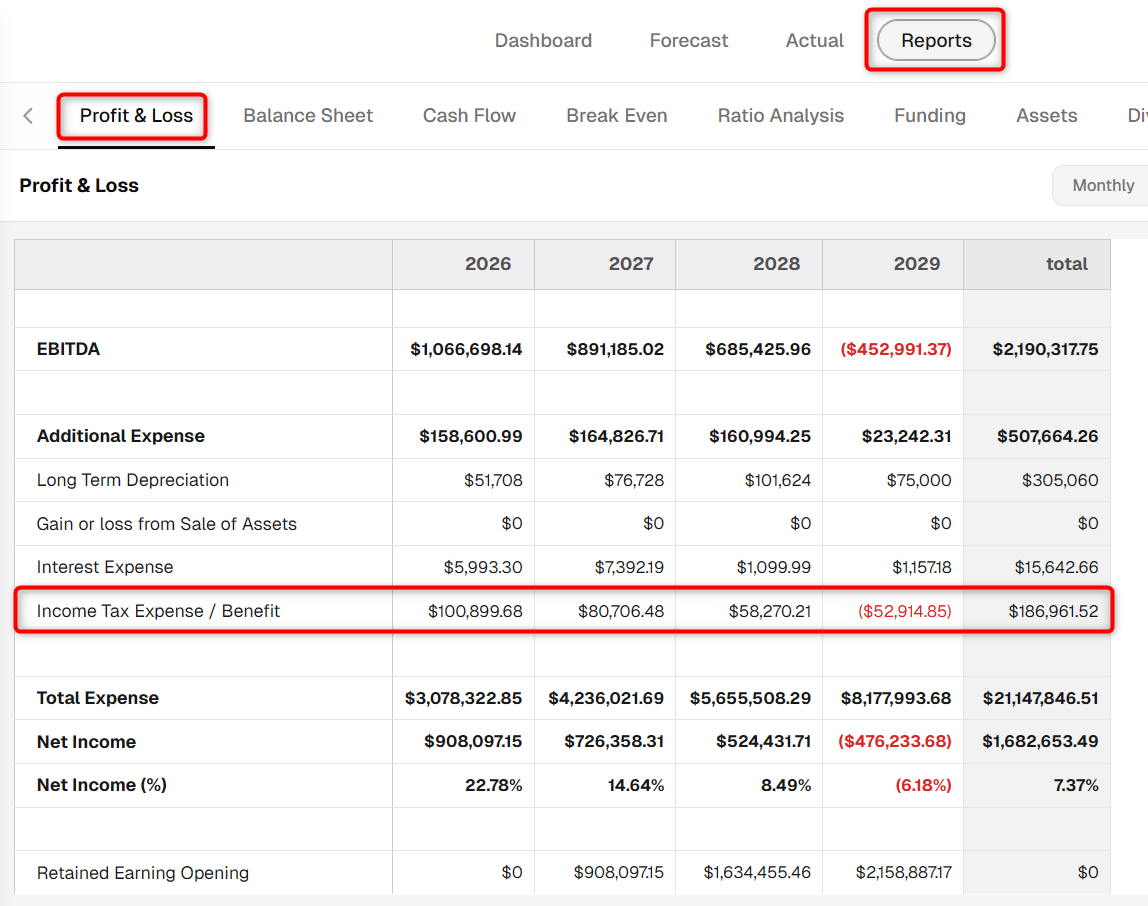

Where does this entry appear in the financial statements?

In the Profit and Loss statement, you will see only income (or corporate) taxes. This is because paying income taxes is an expense of running a profitable business. Sales taxes are not included in a Profit & Loss statement but do appear on the Balance Sheet and the Cash Flow statement.

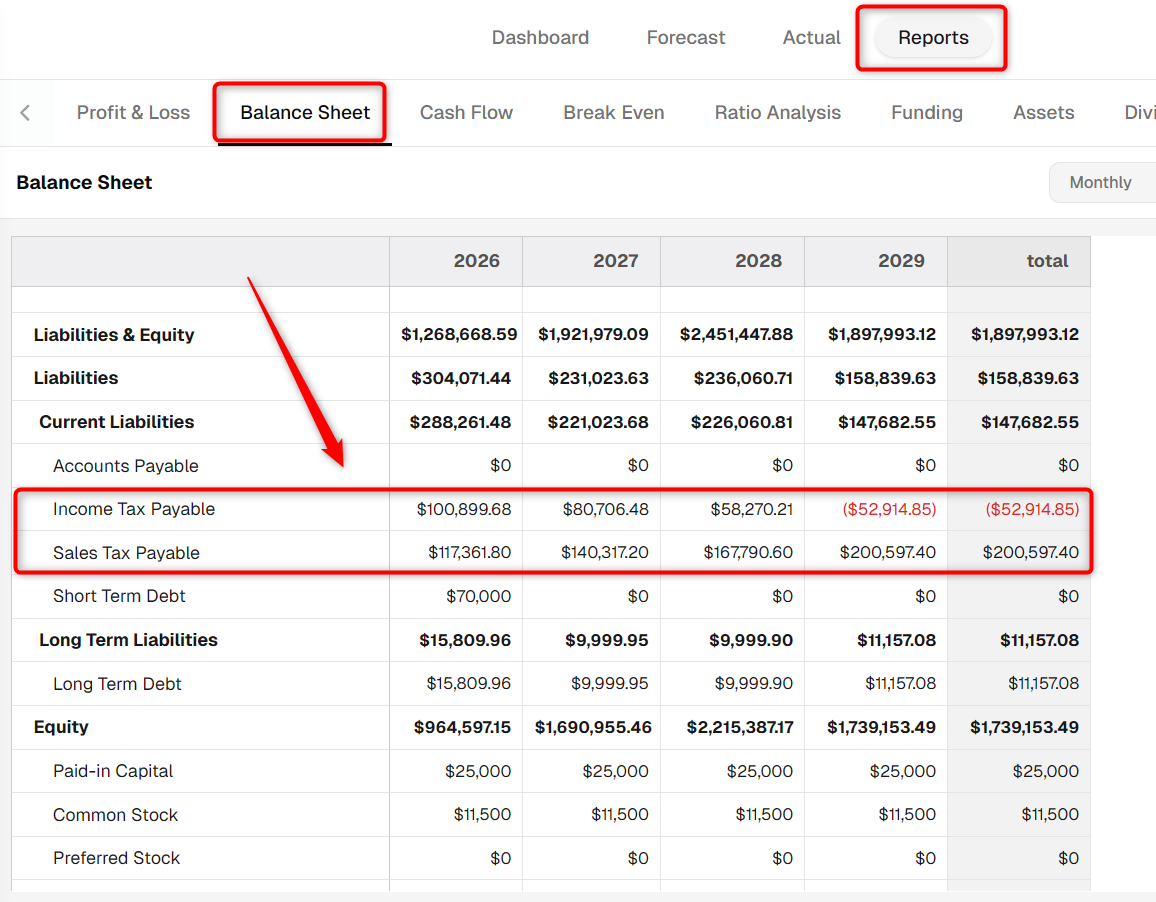

In the Balance Sheet, income and sales taxes are listed as shown below. If you're paying your taxes quarterly or annually, you'll see the amounts increase until the month in which you pay:

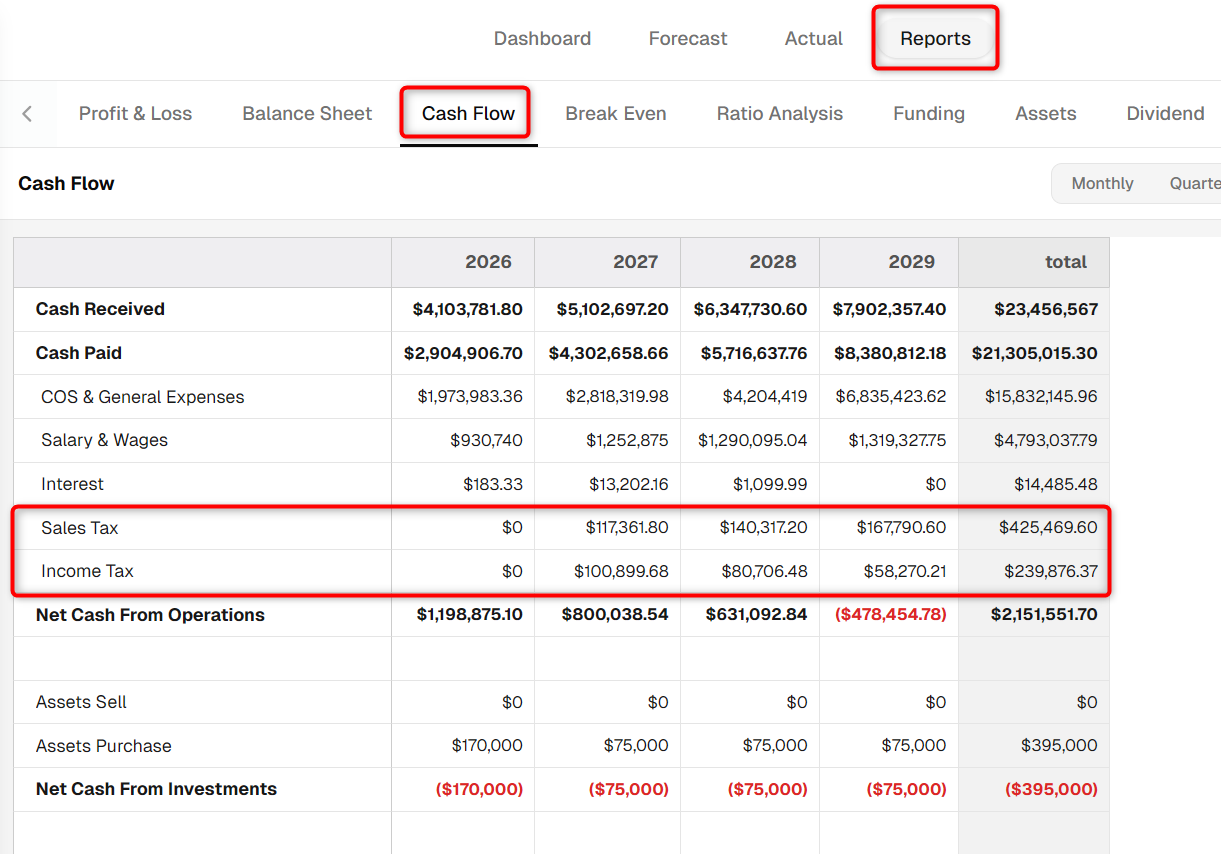

In the Cash Flow statement, you'll see your tax entries expressed as "Sales Tax / Income Tax", meaning the increase or decrease in how much tax you owe in a given month or year. In the example below, we're paying taxes quarterly. So the changes are positive (meaning we owe more) in months where we're accruing taxes and negative in the months in which we pay taxes:

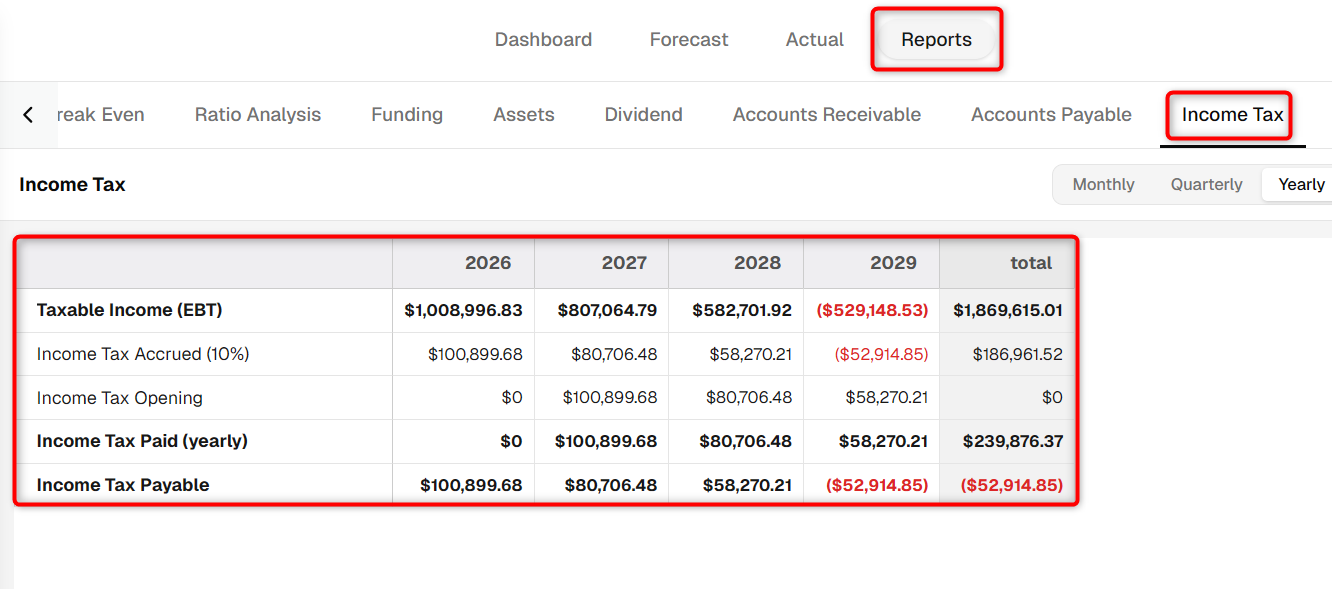

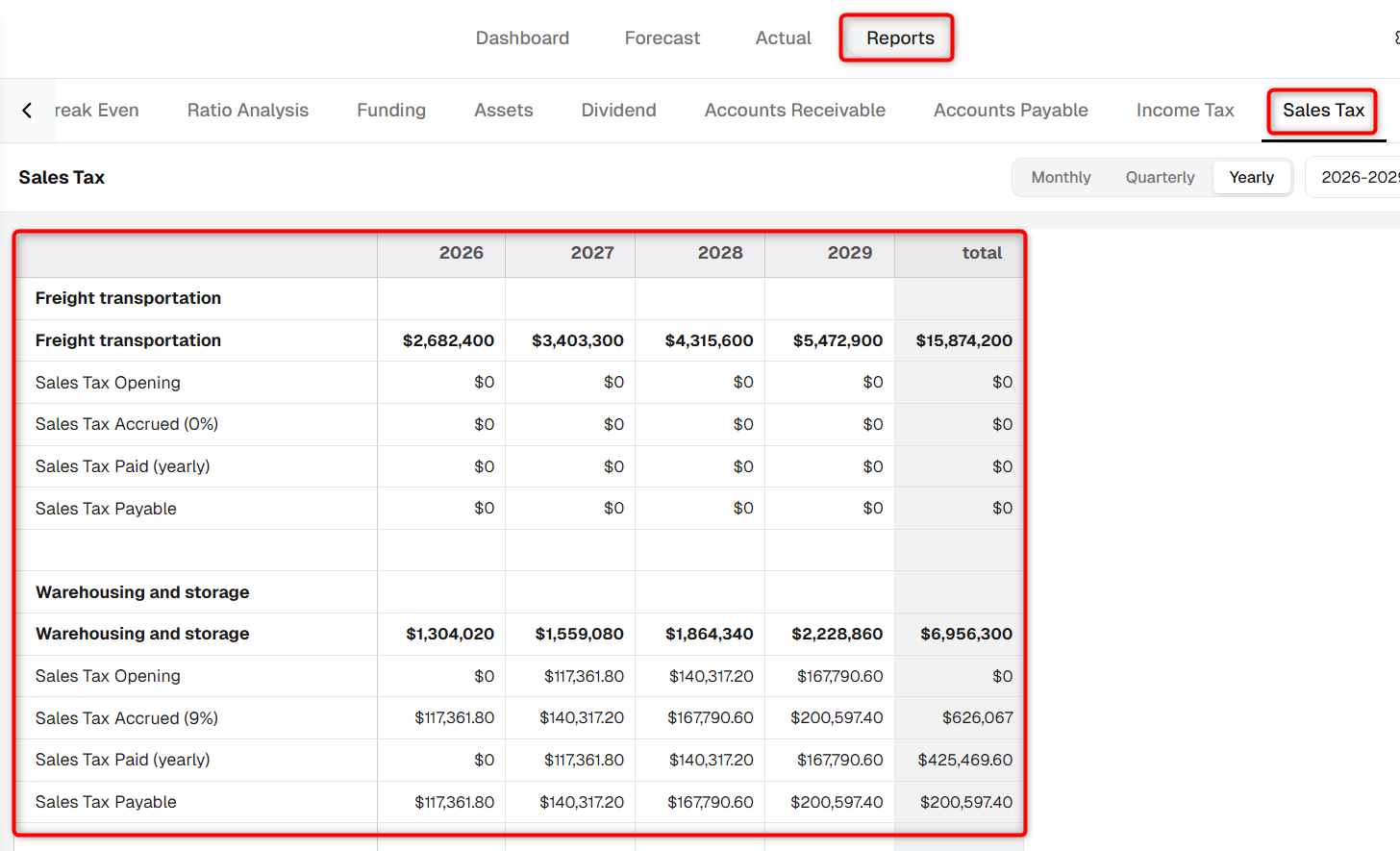

You can refer to the Income and Sales Taxes report for a detailed breakdown of income and sales taxes.